Wash Sale Date Calculator

How to Use the Calculator

In the white dialog box to the right (under Select Date of Sale), input the date of sale in mm/dd/yyyy format or click on the icon on the right of the date input area to use the date picker function instead.

(The Date of Sale is the date when you realized a short or long-term capital loss in a taxable account). Remember, tax loss harvesting doesn’t apply to qualified accounts like IRAs or 401Ks.

As soon as you enter the Date of Sale, the calculator automatically identifies the wash sale window period for that particular security, updates the 3-month calendar UI, and lets you know when it's safe to re-enter that security in light green.

FAQs

-

Tax-loss harvesting involves selling investments at a loss to offset capital gains realized in the current year. If your losses exceed your gains, you can use up to $3,000 of the excess to reduce your taxable ordinary income. Any remaining losses don't disappear—they 'carry forward' indefinitely to offset capital gains in future years.

-

The wash sale rule says that if you sell a security at a loss in a taxable brokerage account (as opposed to a qualified account like an IRA), and buy the same or a “substantially identical” one in any brokerage account within 30 calendar days before or after the sale, the IRS disallows that loss for current‑year tax purposes, and you can't carry forward those losses to offset future capital gains. If you buy that same stock back too soon, the IRS hits the 'Undo' button on your tax break. That’s why the Wash Sale Date Calculator is your best friend.

-

Regardless of your tax bracket, traders and investors can save potentially thousands in capital gains taxes reported on Schedule D (1040). Over the years, you can build up a "tax bank" of realized losses than carry forward indefinitely. This bank can offset up to $3,000 of ordinary income per year and substantially reduce future capital gains taxes from investments in taxable brokerage accounts, real estate, and/or collectibles. In effect, this "tax bank" creates a shield that helps reduce the tax impact of your future wins, allowing you to keep more of your profits.

-

Yes. According to the IRS, there is a hierarchy that you should be aware of:

Short-term losses must first offset short-term gains.

Long-term losses must first offset long-term gains.

Only then can the excess cross over to offset the other type.

The good news is that tax software and IRS forms (Form 8949/Schedule D) automatically handle these netting rules for you. However, you should still be mindful: harvesting a loss to offset short-term gains (taxed at higher ordinary income rates) is significantly more valuable than offsetting long-term gains (taxed at lower rates). Smart traders use apps like Wash Sale Guard to ensure their high-value short-term losses stay in their 'tax bank' rather than being accidentally disallowed.

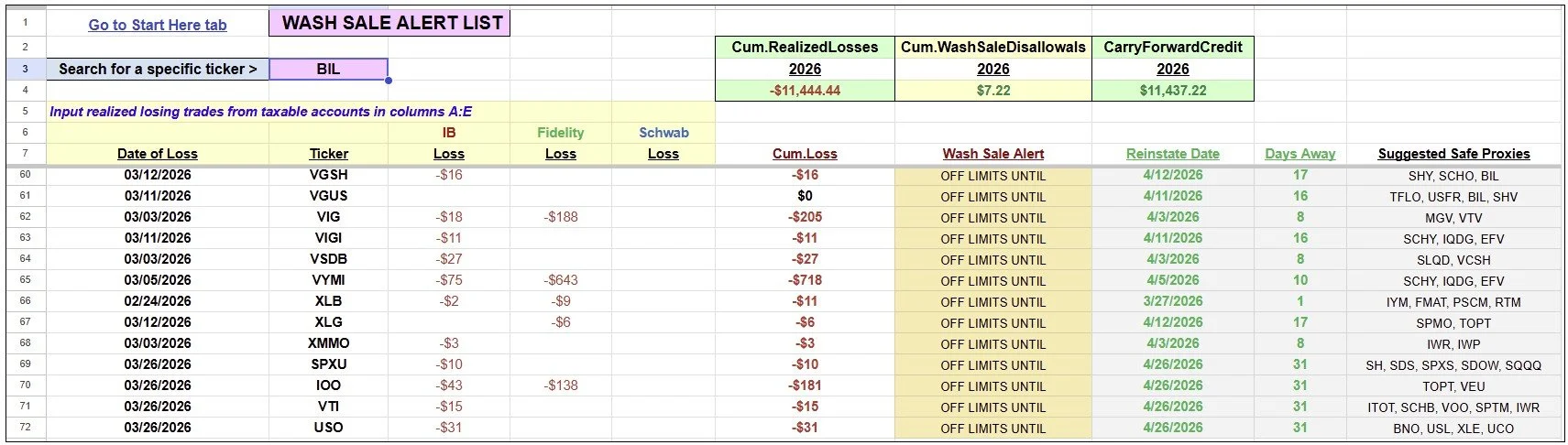

Get the complete Wash Sale Guard App!

It alerts you when you're about to violate the wash sale rule, which tickers are safe to trade and when.

It suggests proxy securities during the wash sale window period.

It also tracks your cumulative carry-forward "tax bank" that you can use to offset future short and long-term gains (as well as ordinary income).

Get the Wash Sale Guard App by clicking here!